Investment background

It is an understatement to say that, from an investor’s perspective, the quarter just passed has been one of very mixed challenges, threats, and outcomes; it has reflected the extraordinary economic and political upheaval markets have faced. However, more encouragingly we have also perhaps witnessed the first stages of the eventual shift in the status of Covid-19 from “pandemic” to “endemic”. But Covid is, of course, still not over.

Our industry has now endured nearly two years of Covid disruption, with pubs being closed, re-opened with restrictions, closed again, re-opened again with different restrictions, and so on. Although people have started to mix more with others and venture out of their homes to visit hospitality and entertainment venues, many still do so with caution, and we are far from returning to the pre-Covid “normal”. We are beginning to learn to live with fewer restrictions. This should result in a more stable environment and, therefore, encourage economic growth: nonetheless, emerging from Covid restrictions and their effect on the economy will be a marathon and not a sprint.

At the industry level, trade has not yet recovered across the board, and many companies continue to have to make adjustments to their business models as customer behaviour changes. For many, even getting sales to pre-pandemic levels will not return them to profit at pre-pandemic levels. This is because they are experiencing very significant cost increases, particularly for energy and labour. This combination of supply chain challenges and labour shortages has contributed to a steep rise in inflationary pressures which, in turn, led to the authorities increasing interest rates at the same time as the government scaled back the support it offered to the industry during the worst stages of the pandemic.

The explosion in energy costs, exacerbated by Russia’s invasion of Ukraine, will be well-known to all of you; the increase in labour costs is widespread across the industry, with many finding it difficult to recruit good staff, particularly in kitchens. Building sales to levels that cover these cost increases would be a challenge at the best of times, and the next 12 months are not likely to be the best of times. This is not just because of the well-publicised hit to the disposable income of customers, due to general inflation, energy costs, mortgage costs, and tax rises. This cost-of-living squeeze will result in families re-assessing their priorities and how they spend their disposable income, which will inevitably depress discretionary spending such as pub visits.

It is also clear that not all of those who were prevented during lockdown from going to the pub are coming back to the pub: this is particularly true of the older population who have traditionally been in the mainstream of cask beer consumption. With less demand for wet led pubs, there is a polarisation in trade developing which might persist. We are beginning to see casualties already though, so far, primarily amongst the smaller brewers. Such failures are due to many factors and whilst some might be solely down to the effect of the pandemic, many are the result of management weaknesses which the lockdowns laid bare.

As far as pub groups are concerned, demand for properties has surprisingly outstripped supply, but recently there have been early signs this is starting to change. The loss of government support and cost pressures are causing more proprietors to consider that it is time to sell. This might accelerate further when the moratorium preventing landlords from evicting tenants for non-payment of rent ends at the end of March.

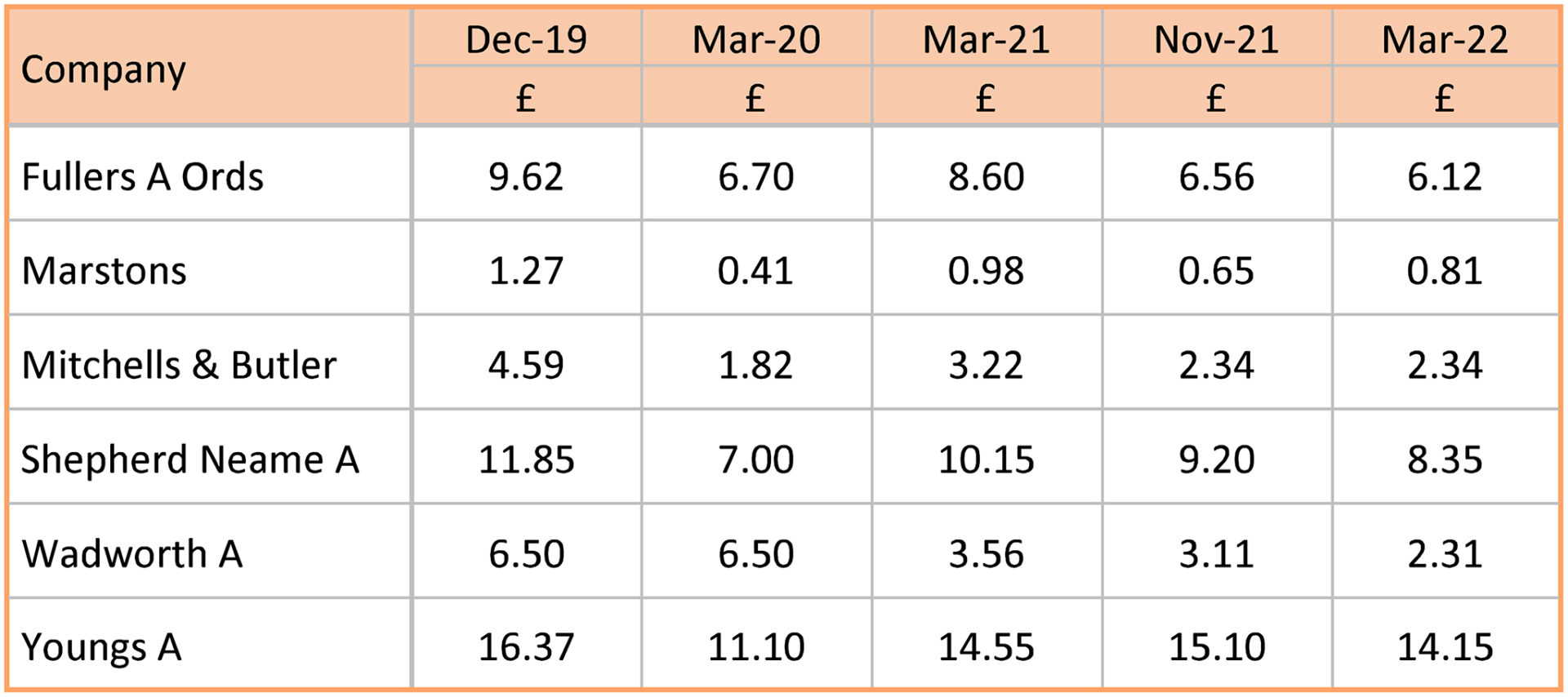

We cannot disguise the rocky road that the Club has travelled since the early days of the pandemic. The decline in unit value reflects the negative background described above. The table below illustrates the share price movements of a handful of the portfolio companies we invest in: –

Unquoted investments and portfolio risk

When the Committee has consulted with members over investing in smaller companies, especially brewers, it has always been strongly supported, notwithstanding the difficulty in identifying sound opportunities and evaluating the risks involved. We have continued to do this but have struggled to find businesses that do not price themselves too highly and/or offer financial returns rather than just product in kind!

We are also conscious of the pressures that Covid continues to bring to this sub-sector. Although investment in an individual smaller company carries a higher risk than investing in a larger one, spreading the risks across a portfolio of smaller companies is only slightly greater than investing in a portfolio of bigger ones. Although the Club does have holdings in major brewers, the overwhelming number of our investments are in what are regarded as smaller UK listed companies. Our principal risks are, therefore, market price risk and liquidity risk. The latter is particularly crucial when evaluating our few holdings in unquoted companies. The Committee has spent much time considering this (especially in light of the failure of West Berkshire) and have decided, therefore, that whilst we will continue to seek out potential investments, we will do so knowing that any investment will be nominal. It is very difficult to evaluate these businesses, especially when the crowdfunding ethos does not seem to include looking for a profitable return. Valuing such businesses is not a perfect science.

Membership news

The gloom also pervades this section of my report because, although we continue to recruit new members, those leaving, I’m sorry to say, outnumber them. We recorded 75 departures and 21 deaths during the year, against 31 joiners. Of those who gave a reason for leaving the Club, the largest group by far stated that they were leaving the Campaign. Please remember that you can “rest” your contributions at any time and leave a residual balance of as little as £20 in the Club.

Administration

I would like to thank all those who have worked steadfastly throughout the year to ensure the smooth running of the Club, including, and in no particular order: Allens, our administrators at Stockport; Hadfields, our reporting accountants; James Sharp and S+T, our brokers; our branch ambassadors; my fellow Committee members and, last but by no means least, you the members for your encouragement and support during this most difficult of times.

Outlook

As I write this piece, I’m only too well aware of the heightened risks and uncertainty investors face, and it is easy to become uncomfortable in these situations. War has returned to Europe. The human cost is already apparent. War also usually heralds higher inflation, and it would be dangerous to conclude that the price rises we are now facing stem purely from the pandemic. Given the unprecedented levels of debt around the world, it is tempting for governments to allow inflation to run at higher levels than we have known because it constrains debt growth. This is, of course, not a policy that can be publicly avowed, but savers need to be aware that it is happening.

More particularly, for your Club being focussed on real ale, our financial returns are very dependent upon the profitability and sustainability of the domestic hospitality sector, and these are under threat. Many have been resilient through the great challenges of the past two years but there are many bumps on the road ahead. While politics and economics will be important influences on the Club’s near term returns, the more important contribution over time stems from the fortunes of its investee companies. Pubs and brewers need to adapt to the new post-Covid trends (such as the increased working from home and greater acceptability of canned beers) if they are to survive and continue to attract the consumer in an age of changes in drinking habits. There will be more casualties along the way. It is encouraging to see positive support for the future of cask ale from some leading producers and the gradual uplift in pub trade since the easing of restrictions.

In the short term, it is important to deal with, understand, and adjust for market movements caused by “macro” factors (the FTSE 250 fell 20% from its all-time high in one week in March) and remain positive. The Bank of England has warned that things won’t get better until 2023 at the earliest. The Club and other investors face volatility, uncertainty, complexity, and ambiguity. As geo-political tensions mount and markets continue to churn, the next couple of quarters are likely to remain fractious. We will be watching matters closely and reacting as flexibly as we can.

Thank you for your continued support.

John Hattersley – Chairman – CAMRA Members’ Investment Club